Chinese consumer purchasing habits have evolved. China has become an ultra-connected country with more than 600 million Internet users and now carried by the e-commerce in all areas. Chinese consumers make more online purchases and physical stores are neglected. However, is it preferable and advantageous for companies and brands to have their online or offline store, or a mix of both?

Chinese consumer trends

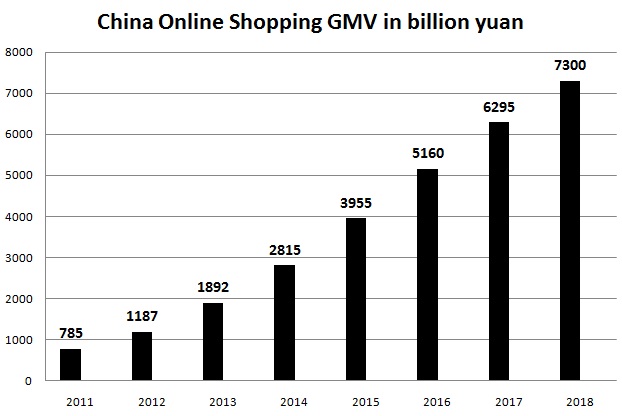

Chinese are the biggest spender in the world and more and more likely to make online purchases. With the most connected people in the world, China has increased from 140 million online shoppers in 2010 to 634 million in 2014. As a comparison, Americans are have gone from 140 million to only 200 million. More than 300 million Chinese consumers have purchased at least once a month on online sites. In 2013, they spent US $ 882.75 million in a day via their mobile phone.

Chinese social networks

91% of Chinese Internet users have an account on one of China’s leading social networks, namely WeChat, Weibo, Renren or QQzone. Unlike Western, Chinese spend their lives on social networks greatly influences their purchasing decisions. They spend a lot of time on social networks (here for a list of the top 5 Chinese social networks) and forums to learn about the products they are likely to buy. They also give more importance to the opinions, comments and advices from their peers on social networks than those left on the official companies or brands’ websites.

Online sales in the booming e-commerce sector

With a penetration rate of 10% and sales online expected to represent 539 billion dollars in 2015, e-commerce is the new place to be for all professionals. According to Forrester Research data in China, online shopping will exceed US $ 1 trillion in 2019. At present, there is no area that does not use e-commerce. Moreover, with the development of applications on mobile to make purchases directly, this trend should further increase.

{kind=link}

Professionals have been able to take this new trend, and increase as Alibaba and his competitor JD.com who became giants of e-commerce. Alibaba owns 60% of market share and JD.com 18.6%.

Physical store

The effects of advanced e-commerce is felt on store owners and physical stores in China. The Chinese have long time preferred shopping stores for the advice of a person. Whether the Chinese sports brand Li Ning Co or the Bloomberg business, they say they have experienced financial difficulties because of the digital transition and some of their outlets had to be closed.

020 strategy

Henceforth, the traditional brands must adapt their marketing strategy to this new way of doing business and combine online and offline to expect attract Chinese consumers and be sustainable. Digital media have become an important key partner for professionals. The O2O becomes the perfect win-win solution for both parties. The goal is to get through the social networks Chinese consumers to come in the physical shop. Many brands have understood and fully integrated into their marketing strategy. This is the case of Mont Blanc, Tag Heur or French cognac company Martel that invites its Chinese customers to come to their physical event through QR code via their accounts on Chinese social networks like Weibo or WeChat.

Promoting stores through digital marketing is critical for Fashion brands in China

Physical retail shops are able to provide a truly unique user experience that online shops can hardly provide : unique events, advice from well-trained staff, particular ambiance.

On the other hand, online shops, on brand websites, e-platforms such as Jingdong or Taobao are able to provide lower prices, premium discounts and so on.

It is not one VS the other here, for the best strategy. The best strategy is to design a plan including both for a very efficient way of having customer purchase your products. Indeed, different types of clients may prefer different different types of customer.

One way or another, only one way to promote your shop : go digital.

As a Fashion brand in China, whether you are a fashion brand that has been in China for a while or a newcomer on the market you must use digital marketing and its tools for greater success.

- A good Baidu strategy on the most relevant keywords to your brand

- A heavy social media campaign, more on social media here

- A good online PR, for more information here

1 comment

Yann.02

Online or physical shops? Why choosing when you can pick both and be more efficient!! Totally agree with O2O strategy, still the cost-efficient strategy to bet on in China. Online to offline is more popular than offline to online but people are more and more wealthy and have less and less time to purchase. A very good article.